Bali off-plan villa investment still attracts global capital, but the market has changed. Demand remains strong, yet supply growth, discounting pressure, and hidden operating costs are exposing weak investment structures. The real question in 2026 is no longer whether Bali has demand. It does. The real question is whether your asset is strong enough to defend occupancy, ADR, and resale value in a market full of similar product.

Too many investors still buy villas as if they were passive real estate. In reality, they are buying operating businesses with revenue risk, cost leakage, legal constraints, and exit friction. That is why the gap between a glossy off-plan promise and real owner returns is often far wider than expected.

TL;DR

- Bali demand is real, but oversupply is putting pressure on many standalone villas.

- A weak Bali off-plan villa investment model can lose pricing power very quickly once real costs hit.

- Professionally managed assets usually perform better because they have stronger distribution, better revenue management, and more resilient commercial logic.

Why is Bali off-plan villa investment under more pressure now?

Because visitor growth is no longer enough to protect undifferentiated assets.

Bali continues to benefit from strong tourism momentum, but short-term rental supply has expanded aggressively. That means more units are competing for the same guest attention, often in the same locations, with similar design language and similar promises. When supply grows faster than differentiated demand, the pressure usually appears in ADR discounting, weaker occupancy consistency, and lower net owner yield.

This is the structural issue behind many disappointing returns. The destination itself may still be healthy, while individual assets underperform badly. That distinction matters.

We made a related point in Bali’s Real-Estate Bubble: Oversupply Threatens Long-Term ROI, where the core warning is simple: rising demand does not rescue weak supply forever.

What is the real problem with many Bali off-plan villa investment models?

The real problem is that many are sold as property first and only later treated as hospitality.

That is backwards. In Bali, returns are driven by operations. A villa may look attractive in a sales brochure, but the actual investment outcome depends on occupancy quality, channel mix, revenue management, maintenance discipline, staffing efficiency, guest reviews, compliance, and resale liquidity.

A large share of weak Bali off-plan villa investment deals fail because the underwriting is built around gross revenue fantasy rather than owner-net reality. Investors are shown best-case occupancy, best-case ADR, and simplified cost assumptions. The commercial risk sits in everything that gets ignored between those slides and the actual P&L.

By contrast, professionally managed assets are usually designed around commercial performance from day one. That difference changes the economics.

Why do professionally managed assets usually outperform?

Because they operate as systems, not isolated units.

A professionally managed hospitality asset has four major structural advantages:

- stronger distribution and channel strategy

- better revenue management and rate discipline

- better cost absorption through scale

- more opportunities for ancillary revenue

This is why managed hospitality formats usually outperform standalone villas over time. They are not relying on one listing, one owner, or one narrow booking logic. They are built to compete.

That same operator-first logic sits behind Zenith’s point of view in The End of the Standalone Villa: Why Integrated Hospitality Is Bali’s Future. If the asset has no real operating advantage, it will eventually be forced into discounting.

Why do so many villa yield promises break down in reality?

Because most headline yields are built from gross revenue logic, not true owner-net cashflow.

This is where many investors get trapped. A project may advertise 15%+ returns, but the real number changes sharply once you include the full cost stack. OTA commissions, management fees, staffing, utilities, maintenance, taxes, repairs, insurance, replacement reserve, and low-season softness all reduce the result.

A villa can look strong on paper and still disappoint badly in practice. That is especially true when the project assumes high occupancy every month, ignores meaningful owner-use costs, or understates the drag created by commercial fees and maintenance.

This is exactly why we often challenge optimistic forecasting in Hotel Feasibility Study Is Wrong: The ADR and Occupancy Fantasy. A forecast is not credible just because it is neatly presented.

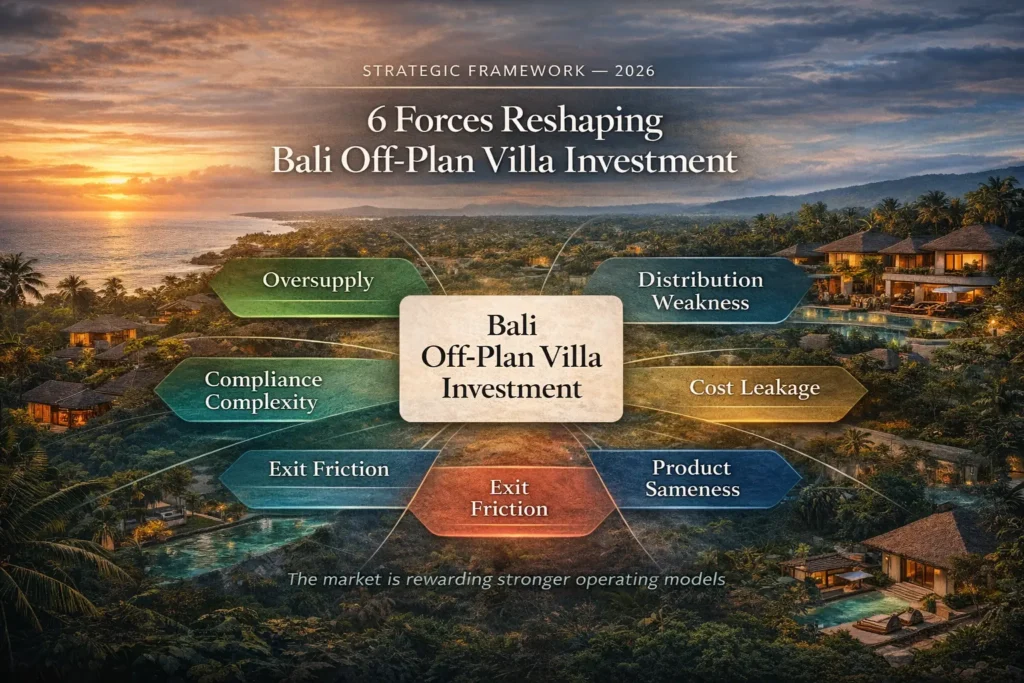

What are the six forces reshaping Bali off-plan villa investment in 2026?

The market is being reshaped by six forces, and every investor should underwrite against all of them.

1. Oversupply

Too many villas are competing in the same booking ecosystem. When product becomes interchangeable, rate pressure follows.

2. Distribution weakness

Many standalone villas rely too heavily on OTAs and weak direct-booking capability. That makes them vulnerable to commission drag and shallow demand quality.

3. Cost leakage

A single villa absorbs maintenance, utilities, staffing support, and commercial friction without the economies of scale that stronger managed assets enjoy.

4. Product sameness

A nice pool, polished stone, and tropical design are no longer enough. In many Bali submarkets, good design is now baseline rather than differentiation.

5. Exit friction

A Bali off-plan villa investment is not just about entry pricing. It is also about how easily you can sell later, under what structure, and with what discount risk if tenure has shortened.

6. Compliance and ownership complexity

Foreign investors still need to treat land structure, licensing, and legal setup with serious discipline. Weak structuring can destroy value even if the villa trades well for a period.

For legal risk, Nominee Structure in Bali — Why Foreign Owners Lose Everything remains essential reading.

What does professional management actually improve?

Professional management improves the asset where most weak investments break: revenue quality, operating discipline, and commercial defensibility.

Revenue quality

Good revenue management is not just “raising rates.” It means seasonality strategy, segmentation, pacing, minimum-stay logic, channel mix control, review conversion, and protecting yield without destroying occupancy.

Operating discipline

Assets perform better when service standards, maintenance routines, reporting, training, and accountability are structured. Weak operations usually show up first in reviews, then in rates, then in net income.

Commercial defensibility

Managed assets can often generate revenue beyond accommodation. F&B, wellness, coworking, memberships, experiences, retail, or club logic all create more resilience than a pure room-night model.

Exit narrative

A buyer is more likely to trust a properly governed operating business than an owner-led rental story with inconsistent records.

That is also why early design decisions matter. We have written about this in Architect Hospitality Consultant Bali: Design That Opens Right and in Pre-Opening SOP Checklist: The Blueprint of Hotel Success. Bad operating logic is expensive to fix later.

Standalone villa vs managed asset: what is the real difference?

The simplest answer is this: one is usually sold as a property unit, while the other is built as a commercial platform.

| Factor | Standalone Off-Plan Villa | Professionally Managed Asset |

|---|---|---|

| Occupancy stability | More volatile | Usually more stable |

| ADR defense | Often discount-led | More disciplined |

| Distribution strength | OTA-heavy | Broader channel mix |

| Cost absorption | Weak | Better scale efficiency |

| Ancillary revenue | Limited | Often diversified |

| Governance | Fragmented | Structured |

| Exit story | More fragile | Usually more credible |

This does not mean every villa is a bad investment. It means the weaker format starts from a weaker commercial base.

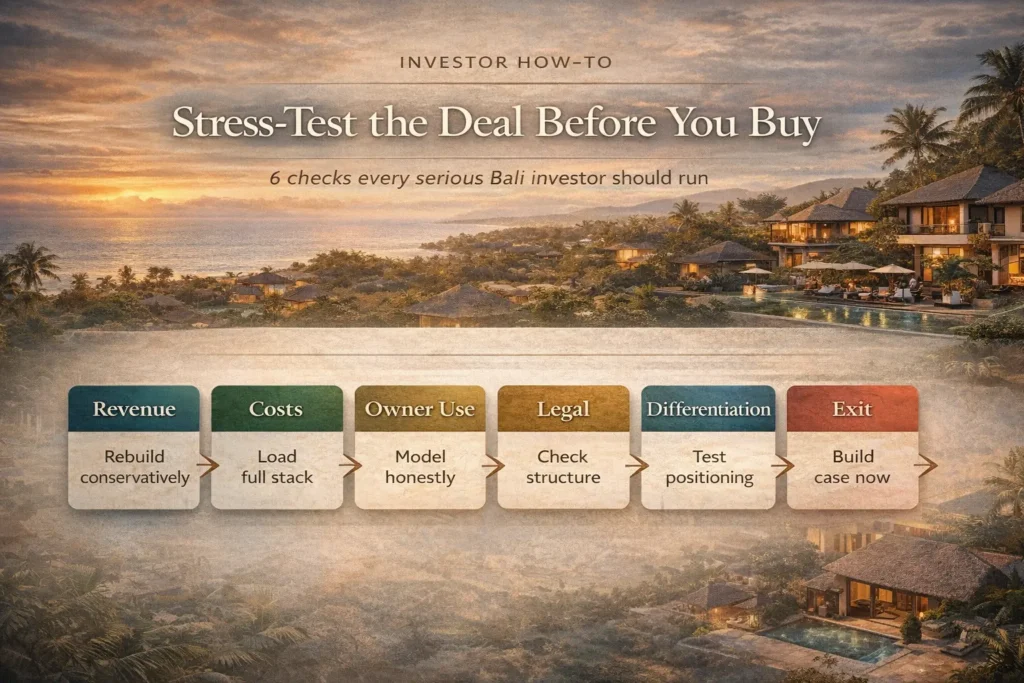

How should investors stress-test a Bali off-plan villa investment before buying?

They should stop underwriting upside first and start underwriting downside first.

A serious investor should assume that some of the sales assumptions are too optimistic. The correct question is not “Can this work if everything goes right?” The correct question is “Does this still work if reality is less generous?”

How to stress-test a Bali off-plan villa investment before you buy

Step 1: Rebuild the revenue line conservatively

Model peak, shoulder, and low season separately. Reduce both ADR and occupancy from the developer case and test a real downside.

Step 2: Load the full cost stack

Apply OTA commission, management fees, maintenance, utilities, staff support, reserve for replacement, insurance, taxes, and compliance costs. Do not bury them inside vague percentages.

Step 3: Model owner use honestly

Owner stays are not free. If they happen during peak periods, they reduce sellable inventory and can materially affect annual yield.

Step 4: Check legal structure and tenure

Clarify whether the asset is leasehold, PMA-linked, or another structure. Review assignment rights, tenure remaining, licensing, and resale constraints.

Step 5: Test differentiation

Ask what genuinely makes the asset harder to replace. If the answer is only “nice design” or “good location,” the moat is weak.

Step 6: Build the exit case now

Estimate how liquid the investment may be in three, five, or seven years. Do not assume a clean resale market if oversupply persists.

For broader market context, investors should also benchmark against more neutral sources such as BPS Bali, UN Tourism, WTTC, and Horwath HTL’s Bali hotel and branded residences analysis.

What should investors buy instead of generic off-plan inventory?

Not “instead of Bali.” Instead of weak product.

That distinction matters. Bali can still be attractive. But a weak Bali off-plan villa investment thesis is very different from a strong hospitality investment thesis. The better play is usually a differentiated, professionally managed asset with clear revenue logic, stronger operating control, and better exit defensibility.

In practice, that may mean:

- a branded or semi-branded hospitality product

- a properly managed villa cluster rather than isolated units

- a retreat or wellness-led concept with genuine differentiation

- a mixed-use hospitality model with ancillary revenue

- an operator-led project built with pre-opening discipline from the start

For investors looking beyond the most crowded patterns, Indonesia Emerging Destination Hotel Investment: The 10 New Balis Opportunity is also worth reviewing.

What should owners and developers do now?

They should become more skeptical, more operational, and more selective.

If you are selling or buying on the assumption that tourism growth alone will carry returns, you are underwriting the wrong market. The next phase of Bali rewards stronger operators, better product logic, cleaner structuring, and more realistic commercial models.

The winners are unlikely to be the most hyped projects. They are more likely to be the projects that can still defend performance after friction, fees, seasonality, and market pressure are applied.

FAQ

Is Bali off-plan villa investment still attractive in 2026?

Yes, but only selectively. Bali remains a powerful destination, but many villa segments are under supply pressure. The right investment is one with real differentiation, realistic underwriting, strong management, and a credible exit path.

Why do professionally managed assets usually outperform standalone villas?

Because they usually combine stronger distribution, better revenue management, better cost efficiency, and more resilient occupancy. They also often generate ancillary revenue that standalone villas cannot.

What is the biggest mistake investors make?

They treat the purchase like passive property rather than an operating business. In Bali, operational weakness usually becomes a financial problem very quickly.

How much do fees really affect villa ROI?

A great deal. OTA commissions, management fees, taxes, maintenance, insurance, and repair reserves can materially compress net returns. That is why gross yield claims should never be accepted without a full net cashflow model.

What should an owner do if they already bought a weak villa asset?

First improve positioning, photography, revenue management, review generation, maintenance standards, and channel strategy. But owners should also stay realistic: operations can improve performance, yet they cannot always fix a structurally weak investment thesis.

Author

André Priebs is CEO of Zenith Hospitality Global, an operator-first hospitality consultancy focused on luxury boutique hotels, lifestyle retreats, and wellness-led assets in Bali and wider Indonesia. He advises owners, developers, and investors on concept strategy, feasibility, pre-opening, operating systems, and commercial performance.

Summary Takeaways

- Bali off-plan villa investment is not automatically broken, but weak standalone product is under growing pressure.

- Oversupply and discounting are making generic villa underwriting more fragile.

- The biggest gap in the market is still the gap between brochure yield and real owner-net return.

- Professionally managed assets usually outperform because they have stronger commercial systems.

- Investors should underwrite downside first, not upside first.

- In Bali, operating model quality is now one of the main drivers of investment quality.

Call to Action

If you are reviewing a Bali off-plan villa investment, do not rely on the developer model alone.

Ask Zenith Hospitality Global to review the deal from an operator-investor perspective: demand realism, ADR and occupancy downside, cost structure, management model, legal setup, and exit defensibility.

Start with Zenith Hospitality Global or explore more analysis in the Zenith Blog.