Bali still has demand. However, it no longer has unlimited room for weak concepts, fragile legal structures, and amateur operations. That is why distressed hotel investment Bali is becoming one of the most interesting opportunity sets for sophisticated buyers.

Today, the market is forcing a separation between strong assets and weak sponsors. In some cases, developers overpromised yields they cannot support. In others, operators can no longer carry lease or fixed-return obligations. Meanwhile, some owners need liquidity because the product was wrong, the structure was wrong, or the execution was wrong. For the right buyer, this creates a clear opening: acquire below replacement cost, diagnose the real failure, reposition the concept, and install professional operating discipline.

The central challenge is simple but difficult. Buyers must separate “wrong concept, salvageable asset” from “fundamentally flawed asset.” Many failed hotels in Bali can be fixed. Just as importantly, many should be avoided.

For related reading, see our analysis of the Bali real-estate bubble and oversupply risk, our guide to hotel licensing in Indonesia for foreign investors, and our piece on why hospitality management contract misalignment destroys value.

Why is distressed hotel investment Bali becoming more attractive now?

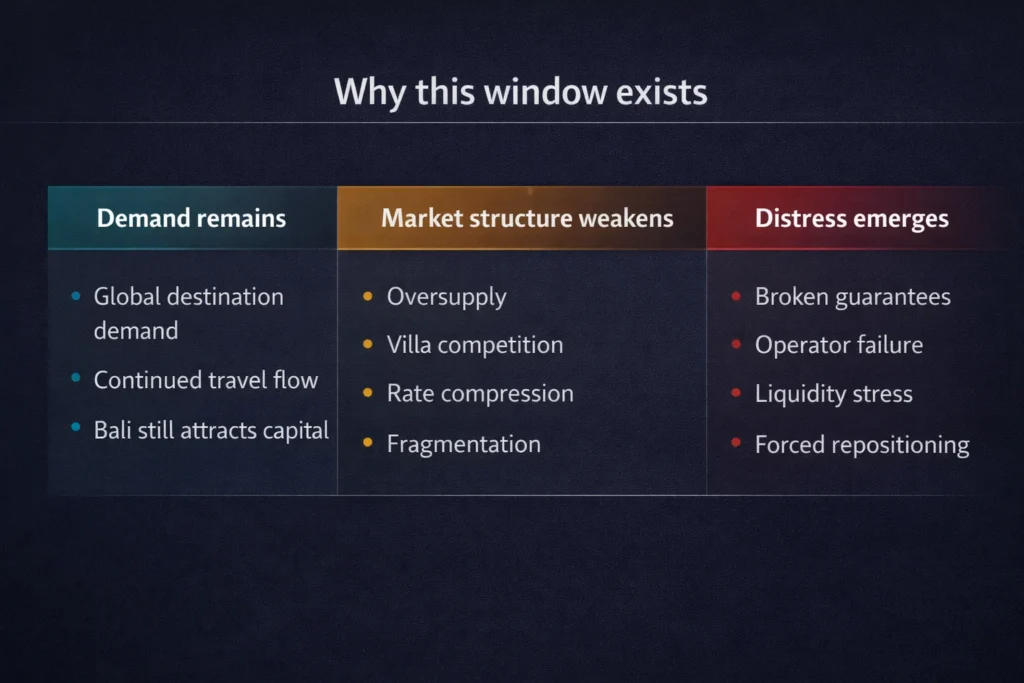

Direct answer: distressed hotel investment Bali is becoming more attractive because demand remains real, while oversupply, villa competition, legal tightening, and broken deal structures are pushing weaker assets into distress.

Bali’s tourism engine is still active. According to BPS Bali, direct foreign arrivals reached 6,948,754 in 2025, up 9.72% year on year, with Australia remaining the largest source market. That matters because distress in Bali is usually not caused by “no tourists.” Instead, it usually comes from capital structure stress, poor product-market fit, compliance failures, and operational weakness. See the official BPS Bali foreign arrivals release.

At the same time, credible market research shows the paradox clearly. Strong demand can coexist with pressure on occupancy and rate when supply expands too quickly or competes badly. For example, Colliers has highlighted this tension in Bali hotel market reporting, especially the pressure created by rapid villa expansion and competitive fragmentation. Review the Colliers Bali hotel market report.

The truth bomb is straightforward: Bali distress is rarely a tourism problem first. More often, it is a structure-and-execution problem first.

What usually causes hotel distress in Bali?

Direct answer: most failed hotels in Bali do not fail for one reason. Rather, they fail because several problems stack at once: wrong concept, weak legal-operating structure, unrealistic return promises, aggressive lease economics, poor revenue management, and no real differentiation against villas.

1. Wrong concept in the wrong micro-market

A hotel can sit on a good island and still be a bad investment. Bali is not one market. Instead, it is a group of very different demand nodes with different guest behavior, price elasticity, and competitive sets.

As a result, a generic hotel in a crowded area with no clear reason to exist will struggle even when the island looks strong on paper. That is why micro-market analysis matters more than broad “Bali is booming” narratives.

2. Villa competition and alternative supply

Hotels in Bali do not compete only with hotels. They also compete with villas, serviced units, branded residences, and, in some cases, unlicensed accommodation that can undercut compliant operators.

Because of that, the turnaround playbook changes. A weak hotel cannot win by discounting alone. It must compete on concept, experience, consistency, and operating quality.

3. Compliance fragility

A physically attractive property can still be a bad acquisition if land rights, zoning, building approvals, or operating permissions are weak. In Indonesia, that means investors must understand the real legal-operability path, not just the sales narrative.

For context, read our article on the hidden cost of illegal villas in Bali. You should also review Indonesia’s building framework under Government Regulation No. 16 of 2021 and land rights framework under Government Regulation No. 18 of 2021.

4. Guaranteed-return and presale failures

Many distressed opportunities come from hospitality-linked real estate products sold with aggressive promises. When actual hotel performance cannot support guaranteed returns, liquidity pressure and investor conflict usually follow.

In practice, this is one of the most common ways a “hotel deal” becomes a distressed asset situation in Indonesia.

5. Operator and contract failure

Some assets are not broken physically. Instead, they are broken commercially. The operator may be wrong, the management agreement may be wrong, the lease structure may be unsustainable, or the reporting discipline may be too weak to expose the problem early.

For that reason, distressed hotel investment Bali is not just an acquisition game. It is an operating capability game.

Where do distressed hotel deals in Bali actually come from?

Direct answer: the best distressed deals in Bali rarely appear as clean listings. More often, they emerge through debt stress, restructuring, unfinished projects, partner disputes, enforcement actions, or operator failure.

In practice, distressed opportunities usually come through four channels:

- Bank and creditor workouts: restructuring, enforcement, or settlement situations.

- Public auction and collateral sales: sometimes partial interests, sometimes real hospitality-linked assets.

- Developer liquidity events: stalled or over-levered projects needing recapitalization.

- Operator default or broken commercial structures: especially where fixed obligations became unsustainable.

Indonesia’s restructuring framework matters here. Buyers who understand PKPU (suspension of debt payment obligations) and insolvency pathways can sometimes buy into complexity rather than wait for a clean asset sale. For reference, see Law No. 37 of 2004 on Bankruptcy and PKPU and the national DJKN auction portal.

There is also a practical point here. If you only monitor broker listings, you will mostly see price discovery. By contrast, if you want real distressed hotel investment Bali opportunities, you need local networks, legal intelligence, and early visibility into broken situations.

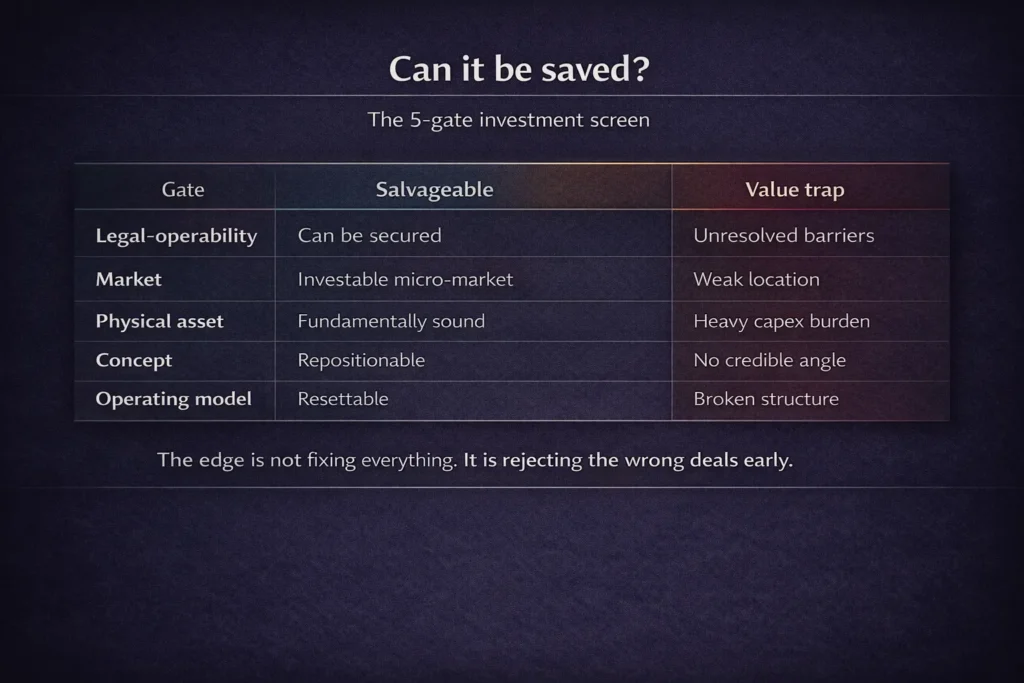

How do you tell a salvageable asset from a value trap?

Direct answer: a salvageable asset has a fixable concept, a workable legal-operability path, sound physical fundamentals, and a realistic route to stabilized NOI. By contrast, a value trap has structural problems that price alone cannot solve.

Zenith’s view is that distressed hotel investment Bali should be screened through five gates.

Gate 1: Can it legally operate?

This is the first filter, not a final checklist item. Confirm the land rights structure, PMA pathway if relevant, zoning exposure, building legality, PBG, SLF, environmental obligations, and hospitality-use permissibility.

If legal-operability is weak, the thesis usually collapses or the price must reset sharply.

Gate 2: Is the micro-market still investable?

A weak hotel in the right node can be fixed. On the other hand, a weak hotel in a structurally poor node is much harder.

Look at access, surrounding demand drivers, F&B ecosystem, congestion, beach or attraction pull, future competing supply, and whether the location fits the repositioned concept you want to build.

Gate 3: Is the physical plant fundamentally sound?

Do not over-focus on cosmetic condition. In many cases, failure starts in MEP, wastewater, water pressure, circulation, fire-life-safety, or service planning.

A hotel with bad finishes can be repaired. By contrast, a hotel with serious technical flaws may consume far more capex than expected.

Gate 4: Can the concept be repositioned into something defendable?

This is the heart of the turnaround. In Bali, “nicer rooms” is usually not enough. The asset needs a sharper reason to win.

That may mean repositioning into wellness, recovery, family, surf-lifestyle, retreat, remote work, or another defendable niche. Even so, the concept must be credible for the location and building, not just fashionable.

Gate 5: Can the operating model be reset cleanly?

Some assets are trapped by fractured ownership, unpaid liabilities, investor disputes, or impossible payout structures. As a result, even a good hotel can fail as an acquisition if the operating platform cannot be cleaned up.

This is where many buyers underestimate execution risk.

What should buyers underwrite in a distressed hotel investment Bali deal?

Direct answer: start with legal-operability, entry basis, capex, time to stabilize, and stabilized NOI. Those five variables usually determine whether the deal works.

A disciplined underwriting model should focus on:

- Entry basis: the real all-in acquisition cost, not just headline purchase price.

- Capex: what is needed to reopen, relaunch, and reposition properly.

- Working capital: especially if the ramp-up period is longer than the seller claims.

- Time to stabilize: a 90-day operational recovery is very different from a 12-month repositioning.

- Stabilized NOI: the number that supports hold yield, refinance, or exit.

The most useful early KPIs are still simple:

- RevPAR = Occupancy × ADR

- GOP margin = GOP / Total Revenue

- Unlevered yield on cost = Stabilized NOI / (Purchase price + Capex + Fees)

Zenith’s practical view is clear: “below replacement cost” only matters if the asset also clears the legal and operational gates. Otherwise, cheap trouble is still trouble.

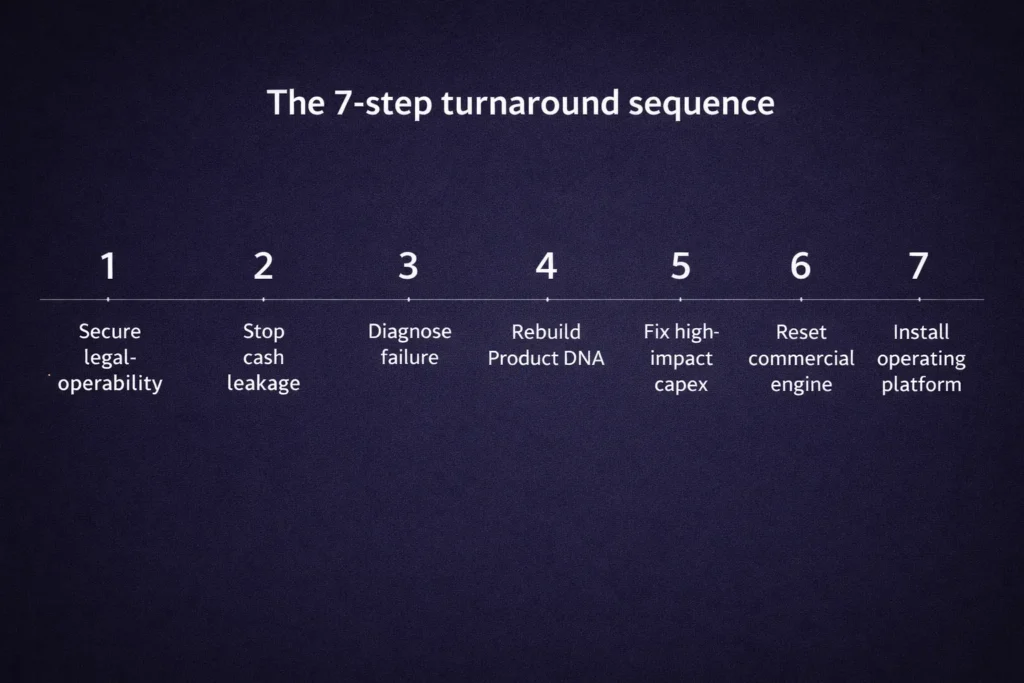

How to execute a hotel turnaround in Bali

A distressed acquisition only becomes a winning investment if the turnaround is disciplined. Below is a practical operator-grade sequence.

How to buy and fix failed hotels in Bali: a 7-step playbook

Step 1: Secure legal-operability before major capital deployment

First, confirm land structure, building legality, PBG, SLF, zoning, tax posture, environmental exposure, and hospitality operating permissions. Do not spend heavily on an asset that still has fundamental legal questions.

Step 2: Stop cash leakage immediately

Next, freeze non-essential spend. Review procurement, staffing efficiency, vendor terms, maintenance priorities, and channel losses. A turnaround often starts by controlling the bleed before chasing upside.

Step 3: Diagnose the real failure

Then separate cosmetic issues from structural issues. Was the hotel hurt by the wrong concept, the wrong operator, weak pricing discipline, poor guest experience, weak compliance, or a bad commercial structure?

Do not prescribe renovation before diagnosis.

Step 4: Rebuild the Product DNA

At this stage, the asset needs a sharper market identity. In Bali, generic stock is vulnerable. The repositioning must answer who the guest is, why they choose this property, and why the experience is different from nearby hotels and villas.

This is where concept strategy and operating strategy must align.

Step 5: Fix the highest-payback capex first

Then prioritize investments that directly affect guest conversion, satisfaction, and rate integrity:

- bathrooms

- bedding and sleep quality

- acoustic privacy

- Wi-Fi reliability

- water pressure

- thermal comfort

- arrival and public-area experience

Do not waste early capex on design vanity.

Step 6: Reset the commercial and operating engine

After that, rebuild the operating core. Turnarounds are not won only with design. They are won with pricing discipline, better channel mix, stronger content, improved SOPs, better training, and owner-grade weekly reporting.

For adjacent thinking, read our analysis of hotel F&B profitability and operating leakage.

Step 7: Install the right operating platform

Finally, install the structure that prevents repeat failure. That may mean a new operator, white-label management, a management agreement reset, or structured owner oversight with asset-management support. The goal is not just reopening. The goal is preventing future distress.

What does “below replacement cost” actually mean in Bali?

Direct answer: in Bali, “below replacement cost” should mean that total basis—purchase, capex, fees, and working capital—is materially below verified replacement cost for that asset type and location, while still leaving room for legal cleanup, repositioning, and stabilization risk.

A disciplined buyer should not use replacement cost as a slogan. Instead, it should be treated as a tested range backed by local construction logic and asset-specific due diligence.

As a practical rule, distressed hotel investment Bali only becomes compelling when:

- the all-in basis is clearly below realistic replacement cost;

- the asset clears legal-operability gates;

- the turnaround thesis does not rely on fantasy ADR growth; and

- the operational upside is achievable with real execution, not hope.

What are the biggest mistakes buyers make?

Buying the discount instead of the thesis

A low price is not an investment case. It is an entry point.

Underwriting Bali as one market

Node-level demand matters more than island-level headlines.

Treating compliance as a post-closing issue

That mistake can destroy financeability, operations, and exit value.

Confusing renovation with repositioning

Paint, furniture, and styling do not automatically create a stronger hotel.

Assuming the legacy structure can remain intact

Some assets need a full reset of the commercial and operating model, not a gentle handover.

FAQ

Is distressed hotel investment Bali mainly a legal play or an operating play?

It is both, but the legal side comes first. An asset that cannot be operated cleanly under the right land, permit, and entity structure is not a true turnaround platform. Once that foundation is secure, most value creation comes from operations: concept reset, pricing discipline, distribution strategy, staffing efficiency, SOP quality, and tighter owner governance. Buyers who are strong only in acquisitions usually miss where the real value is created.

Can foreign investors participate in distressed hotel deals in Bali?

Yes, but the structure must be compliant. The right pathway depends on whether the buyer is acquiring an asset, shares in an operating company, creditor exposure, or some form of recapitalization position. In Indonesia, structure is not a technical footnote. Instead, it shapes control, legality, tax exposure, and exit flexibility. That is why foreign investors need local legal, regulatory, and operating intelligence before issuing an LOI.

Are all failed hotels in Bali worth trying to fix?

No. Some are value traps. The usual reasons include weak land or permit structure, structurally poor location, fragmented ownership, unresolved disputes, or a physical plant that needs irrational capex. The edge in distressed hotel investment Bali is not trying to rescue everything. Rather, the edge lies in rejecting bad deals quickly and deploying capital only where the asset, market, and turnaround path line up.

What should an investor review before making an offer?

At minimum, review land and ownership documentation, PBG and SLF status, zoning exposure, environmental and tax issues, current contracts, staffing liabilities, vendor arrears, historical trading, channel mix, capex backlog, and realistic time to stabilize. In addition, stress-test whether the repositioned concept fits the micro-market. In Bali, many acquisitions fail because buyers underwrite the building but not the operating reality.

Summary Takeaways

- Distressed hotel investment Bali is rising because weak structures are failing faster than demand is weakening.

- The best opportunities usually come from debt stress, broken guarantees, unfinished projects, or operator failure, not polished listings.

- The first filter is legal-operability. Without that, the deal is usually a trap.

- The real turnaround question is whether the asset is fundamentally sound but commercially wrong, or fundamentally flawed.

- Value is created through diagnosis, repositioning, and operating discipline, not through cheap entry alone.

- Sophisticated buyers win by combining local market intelligence with professional hospitality execution.

Call to Action

If you are evaluating a failed, stalled, or underperforming property, Zenith Hospitality Global can help you assess whether it is a genuine turnaround opportunity or a value trap. We support investors with deal evaluation, acquisition due diligence, concept viability assessment, repositioning strategy, turnaround execution, and operator placement.

Before you price the asset, review the structure, the micro-market, and the operating path. That is where the real investment decision sits.

Author

André Priebs is CEO & Co-Founder of Zenith Hospitality Global, an operator-first hospitality consultancy and operating partner focused on luxury boutique hotels, lifestyle retreats, and wellness assets in Bali and across Indonesia. Zenith advises owners, developers, family offices, and opportunistic investors on concept strategy, pre-opening governance, operating systems, commercial performance, distressed asset evaluation, and hotel turnaround execution.