Indonesia emerging destination hotel investment is entering a new cycle. Government-backed tourism development is shifting attention beyond Bali into ten priority destinations where infrastructure, policy support, and early-mover positioning are reshaping the hospitality landscape.

The downside is also real: copying Bali’s assumptions into markets that do not yet have Bali’s demand depth, labor pool, utilities reliability, or regulatory maturity.

If you are serious about Indonesia emerging destination hotel investment, this guide gives you a practical, operator-grade entry strategy across all ten “New Balis”—plus the non-hotel asset classes that often create the real moat.

TL;DR — Key takeaways (for investors, developers, asset managers)

- First, the “10 New Balis” are not one market. Each destination has a different demand engine (culture, nature, events, diving, weekend drive market, etc.).

- Next, the fastest way to lose money is Bali template thinking: Bali ADR, Bali ramp-up, Bali staffing, Bali distribution assumptions.

- Critically, winning assets are small-to-mid scale, differentiated, and operationally realistic, with utilities/water/waste solved on-site and culture integrated from day one.

- Finally, the best strategy is usually a portfolio thesis (2–3 priority bets + 2 optionality bets), not a single “all-in” project—especially in Indonesia emerging destination hotel investment.

What does “10 New Balis” actually mean?

Indonesia’s “10 New Balis” (also called “priority tourism destinations”) is a policy-driven push to accelerate tourism infrastructure, promotion, and investability beyond Bali. The label appears across multiple government communications and has evolved over time (e.g., “10 priority” vs “super priority” subsets). A useful reference point is Indonesia’s Cabinet Secretariat framing of the initiative.

Reference: Indonesia Cabinet Secretariat on building “10 new destinations”

Investor reality: treat the label as directional policy support, not a guarantee of stabilized demand.

The 10 destinations (the “10 New Balis” set)

This is the ten-destination set most consistently referenced in “New Balis” contexts (often with minor naming variations by province / park authority):

- Lake Toba

- Tanjung Kelayang (Belitung)

- Tanjung Lesung

- Kepulauan Seribu (Thousand Islands)

- Borobudur

- Bromo–Tengger–Semeru

- Mandalika (Lombok)

- Labuan Bajo (Komodo gateway)

- Wakatobi

- Morotai

If you want a broader Indonesia-wide baseline, start at the official tourism ministry portal and then go destination-by-destination from there.

Reference: Kemenparekraf / Ministry of Tourism portal

The core mistake: “Bali template thinking” (and why it breaks)

Most failed projects in emerging destinations follow the same pattern:

- Typically, the concept is generic (“luxury resort + spa + beach club”).

- Then, the model assumes Bali-like ADR and a smooth 24–36 month ramp.

- Meanwhile, the operating plan assumes Bali-like talent availability, vendor depth, and utilities stability.

- In reality, the destination runs on seasonal demand, access friction, staffing scarcity, and infrastructure gaps.

- As a result, the project faces rate pressure, channel dilution, service inconsistency, and delayed stabilization.

Therefore, if your feasibility still treats ADR and occupancy as fixed certainties, start here before you deploy capital:

Hotel feasibility study is wrong: the ADR and occupancy fantasy

Zenith’s “Win Without Repeating Bali” framework (6 investor tests)

Use these tests before you buy land, finalize concept, or sign an operator. In practice, these six tests prevent expensive concept drift and force early clarity on demand, operating constraints, and exit:

- Demand Engine Test — What is the destination’s primary demand driver today (not “in five years”)?

- Access & Friction Test — Flights, drive time, port reliability, seasonality, cost-to-arrive.

- Utilities Reality Test — Water, waste, wastewater, power redundancy: solved on-site or not investable.

- Culture & Permission Test — Local norms, community benefit design, religious calendars, land stakeholder map.

- Labor & Service Test — Where does management talent come from? Housing? Training pipeline?

- Exit & Liquidity Test — Who buys this asset later, and what cap-rate reality exists outside Bali?

Moreover, these checks are fastest when run as a single integrated decision gate, not as isolated advisor opinions. If a project fails two or more tests, you do not “fix it with design.” You re-scope, phase, or walk away.

A common failure mode is designing beautiful spaces that cannot be operated (BOH, flow, compliance). If you want the operator’s lens early, this is relevant context:

Architect hospitality consultant Bali: design that opens right

Destination-by-destination strategy (hotels/resorts + adjacent asset classes)

The goal here is not to list attractions. It’s to outline what can win commercially without triggering Bali’s downside externalities.

1) Lake Toba — “Landscape + culture” (but utilities-first)

What wins in hotels/resorts

- 30–80 key nature-led resort with strong view control, cold-climate comfort, and quiet luxury

- Small wellness lodge / recovery retreat built around climate, hiking, and cultural programming (not “Bali yoga clone”)

Adjacent asset classes

- Scenic F&B (destination dining with viewpoint capture)

- Lakeside mobility: docks, small ferries, curated excursions

- Workforce training partnerships (service quality becomes a moat)

Key risk

- Infrastructure gaps can force high CAPEX for water/waste solutions—budget it early, not “later.”

2) Tanjung Kelayang (Belitung) — “Beach + domestic fly market” with boutique upside

What wins

- 40–120 key beachfront resort with high design identity and strong family/wedding capture

- Boutique villas with professional management (avoid informal rental chaos)

Adjacent asset classes

- Branded beach dining + sunset bar (profit-led, not vibe-led)

- Water activities operator (island-hopping, snorkeling, private charters)

- Small MICE/event pavilion (Jakarta corporate offsites)

Key risk

- Overbuilding “midscale boxes” compresses ADR quickly—differentiate or get commoditized.

3) Tanjung Lesung — “Jakarta proximity” (weekend market economics)

What wins

- Short-stay optimized resort (fast check-in/out, family programming, strong weekend yield control)

- Hybrid resort + day-pass model (when executed with capacity discipline)

Adjacent asset classes

- Beach club (controlled capacity, not unlimited external crowds)

- Theme / attraction partnerships (only if demand is proven, not speculative)

- Toll-road-linked roadside F&B concepts (capture drive traffic)

Key risk

- Weekend-only demand creates midweek occupancy holes—your cost structure must survive midweek softness.

4) Kepulauan Seribu (Thousand Islands) — “Near-city islands” (high frequency, low length-of-stay)

What wins

- Small eco-resorts and private-island style inventory with strict waste/water controls

- Premium day-use wellness and “one-night reset” products (Jakarta stress escape)

Adjacent asset classes

- Marinas, charters, water transport scheduling

- Waste/logistics infrastructure (often the real bottleneck—and a monetizable service)

Key risk

- Environmental constraints and waste management are non-negotiable; reputational risk is high.

5) Borobudur — “World heritage gravity” (culture-led, low-noise premium)

What wins

- Heritage-luxury lodge: meditation, learning, sunrise access logistics, cultural curation

- Small wellness retreat with strong “quiet rules” and high perceived value (sleep, recovery, rituals)

Adjacent asset classes

- Cultural F&B (chef-led, ingredient story, craft)

- Learning experiences: workshops, guided culture, philanthropic tie-ins

Key risk

- “Generic luxury resort” concepts underperform—this is a meaning-driven market.

Reference: Borobudur Temple Compounds (UNESCO World Heritage)

6) Bromo–Tengger–Semeru — “Sunrise + volcanic landscape” (time-windowed demand)

What wins

- Small lodge clusters (20–60 keys), strong thermal comfort, curated sunrise mobility

- Glamping done properly (service discipline + weather resilience)

Adjacent asset classes

- Transport and time-window logistics (jeeps, staging, ticketing partnerships)

- Warm F&B hubs (high-margin comfort dining; weather-driven demand)

Key risk

- Weather seasonality + logistics friction: your operating model must be designed for it.

7) Mandalika (Lombok) — “Event spikes + long-term resort corridor”

What wins

- Phased resort strategy: start with a “base hotel” that survives quiet months, expand with villas/experiences later

- Surf + wellness hybrid: low-impact, culturally aware, operationally lean

Adjacent asset classes

- Wellness + recovery clinics (non-hospitality medical must be structured carefully)

- F&B clusters that serve both guests and destination visitors (but capacity-controlled)

- Sports/event infrastructure partnerships (only with demand contracts, not hope)

Key risk

- Event-driven spikes can trick feasibility models into overestimating stabilized demand.

Reference: ITDC update on Pullman Lombok Mandalika

8) Labuan Bajo (Komodo gateway) — “Nature luxury under conservation pressure”

What wins

- 25–80 key luxury eco-lodge or waterfront boutique with strict sustainability systems

- High-yield, low-key inventory that monetizes curated excursions (not mass tourism volume)

Adjacent asset classes

- Liveaboards, dive operators, premium charter services

- Waste and water infrastructure (constraint = opportunity)

- MICE micro-play (small executive retreats, not convention scale)

Key risk

- Conservation scrutiny is high. If your project is perceived as extractive, you will face operational and reputational headwinds.

Reference: Komodo National Park (UNESCO World Heritage)

9) Wakatobi — “Diving world-class” (specialist demand, high willingness to pay)

What wins

- Dive-led eco resort with strong marine partnerships and premium guiding

- Ultra-specialist experience packages (photography weeks, marine biology weeks)

Adjacent asset classes

- Liveaboard docking + provisioning

- Marine conservation partnerships (funding, education, reef monitoring)

Key risk

- Access constraints mean you must design for longer stays and higher value per guest, not high turnover.

10) Morotai — “Remote frontier” (optionality bet, not a base-case underwriting story)

What wins

- Small expedition lodge (20–50 keys) with high self-sufficiency

- Niche positioning: diving + history + “end-of-the-map” storytelling

Adjacent asset classes

- Air/sea logistics, provisioning, micro-infrastructure

- Guides and experience IP (the story is part of the asset)

Key risk

- The market can mature slower than investor timelines; phase CAPEX and avoid oversized fixed costs.

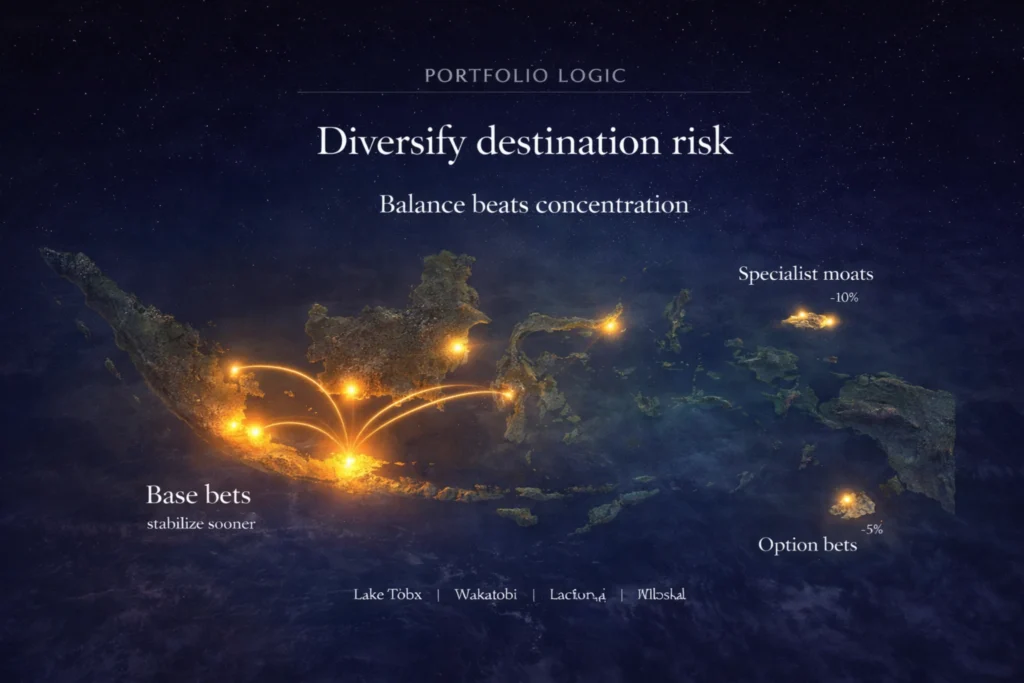

Portfolio strategy: how professionals allocate across emerging destinations

If you are underwriting Indonesia emerging destination hotel investment as a platform (not a one-off), a practical allocation approach is:

- 2–3 “Base bets” (nearer-term demand engines): Mandalika, Borobudur, Labuan Bajo

- 1–2 “Domestic frequency” plays: Tanjung Lesung, Kepulauan Seribu

- 1–2 “Specialist moats”: Wakatobi (dive), Bromo (time-window landscape)

- 1–2 “Option bets”: Morotai, Lake Toba (depending on infrastructure reality)

Rule: The more remote the destination, the more your model must shift from “volume” to “value-per-guest” and from “fixed costs” to “variable, phased growth.”

For the cautionary backdrop on why “destination success” can destroy ROI when supply outruns demand, this is relevant reading:

Bali’s real-estate bubble: oversupply threatens ROI

How to enter an emerging destination (Zenith 90-day market entry playbook)

To move faster while reducing downside risk, run the entry process in this sequence; otherwise, you’ll over-design before the destination fundamentals are verified.

First — Define the destination thesis (Week 1–2)

- Primary demand engine (today vs “future”)

- Target guest psychographics (who buys this, why, and what do they refuse?)

- Competitive set reality (not OTA fantasy)

Next — Build a concept that fits the local ecosystem (Week 2–4)

- Product DNA: promise, signature rituals, service style, spatial logic

- Culture integration plan (community participation, local crafts, calendar, etiquette)

- Sustainability systems as core design inputs (not a marketing layer)

Then — Underwrite with downside realism (Week 4–7)

- ADR/occupancy as probability ranges (base/downside/tail)

- Utilities CAPEX (water/waste/power redundancy) included from day one

- Labor plan: recruitment geographies + training cost + housing strategy

After that — De-risk land and licensing (Week 6–10)

- Title and zoning validation (directly with authorities, not seller claims)

- Environmental approvals pathway mapped early

- Phasing plan aligned to permit milestones (reduce stranded CAPEX risk)

Finally — Lock a go-to-market engine (Week 8–12)

- Distribution strategy (not “we’ll do Instagram”)

- Experience partnerships (boats, guides, culture, mobility)

- Operating model with KPI discipline (service quality, margin, capacity)

If you want the “Bali mistake prevention” lens in a structured, implementation-ready way, this is the closest parallel framework from our library:

Overcrowding in Bali tourism: action plan

FAQ (investor + operator-ready)

Is “Indonesia emerging destination hotel investment” less risky than Bali?

It can be less competitive than Bali, but not automatically less risky. Emerging destinations often have less rate competition, yet higher execution risk: access friction, limited labor depth, and utilities gaps. The right question is whether your concept and cost structure can survive downside seasons and slower ramp-up without discounting your brand.

What’s the biggest mistake foreign investors make in “10 New Balis” markets?

They import Bali assumptions: Bali ADR, Bali occupancy ramp, Bali staffing quality, and Bali supplier reliability. Frontier markets punish speed without operational groundwork. If your model cannot survive a multi-year soft period, the project is not investment-grade.

Which asset classes outperform hotels in emerging destinations?

Often: destination F&B with viewpoint capture, marine/transport operators (charters, dive, logistics), and utilities-linked infrastructure solutions (waste, water, provisioning) because they solve bottlenecks that every hotel suffers from. Hotels win when paired with these moats.

How should developers phase CAPEX in a frontier destination?

Open with the smallest viable “proof product” (boutique lodge / first phase keys) that can run profitably at conservative occupancy. Expand only after: access reliability improves, demand shows repeatability, and the operator demonstrates service consistency. Phasing is not caution—it is strategy.

What does “culturally appropriate” actually mean in practice?

It means the concept earns local permission: respectful design language, community benefit mechanisms, local hiring and training, and behavior rules aligned to local norms. Cultural fit is not decoration; it is risk management that protects operations, reviews, and long-term license to operate.

Summary Takeaways

- The “10 New Balis” are 10 different business models, not one national story.

- Winning in emerging destinations requires operator-grade realism: utilities, labor, access, seasonality.

- Don’t chase scale. Build differentiation + sustainability + disciplined capacity.

- Underwrite downside first, then earn upside through phasing and proof.

Call to action

If you are evaluating a site or concept in any of the “10 New Balis” destinations, Zenith provides an emerging destination market entry strategy: destination thesis, concept/Product DNA, operator model, downside underwriting, licensing roadmap, and phased rollout plan.

For the broader Zenith knowledge base, you can browse the full library here:

Zenith Blog

Author

Zenith Hospitality Global

Operator-first hospitality advisory supporting owners, developers, and investors to design and launch luxury boutique hotels, lifestyle retreats, and wellness/longevity assets—built for real-world operations, not just renders.